If you want to fix up your kitchen or repair a leaky roof without putting your house at risk, an unsecured personal loan is probably your best bet. These loans give you a lump sum of cash upfront based on your creditworthiness rather than the value of your property.

I once talked to a neighbor who spent three years saving for a bathroom remodel. Before he could even break ground, the cost of materials doubled. He ended up taking out a loan anyway, and honestly, the peace of mind from having the cash ready to go was worth more than the interest he paid.

Renovating a home is a massive undertaking that often requires more liquidity than a standard savings account can provide. You might find yourself staring at a stack of contractor quotes, wondering which financing route makes the most sense for your budget and long-term goals.

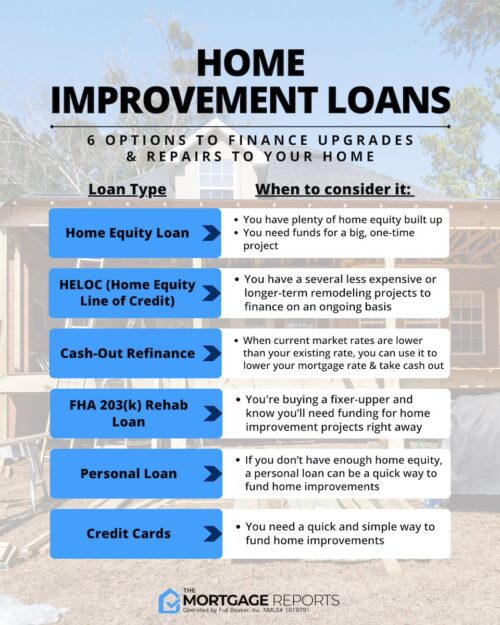

There are a few ways to pull this off. You can use a home equity loan, which uses your house as collateral, or you can opt for an unsecured personal loan, which keeps your property out of the line of fire if things go sideways.

Choosing the Right Amount of Cash

The first hurdle is deciding how much money you actually need to finish the job. It’s easy to underestimate the cost of permits, unexpected plumbing issues, or that specific backsplash tile that suddenly goes out of stock. I’ve seen many DIYers start a project thinking they need $5,000, only to find themselves $10,000 deep by the time the drywall is up.

If you are planning a minor repair, like a new dishwasher or a quick coat of paint, a smaller loan might suffice. But if you’re looking at a full kitchen overhaul or a basement conversion, you might need something much more substantial. Some lenders cater specifically to these larger, more ambitious projects by offering significantly higher limits.

For instance, high-limit personal loans offer fast, unsecured funding up to $100K+ for home improvements without you ever having to risk your home equity. This is a game changer for people who want to increase their property value through major renovations but don’t want to deal with the paperwork and appraisal requirements that come with a second mortgage.

When you look at your options, remember that “unsecured” is the word of the day. This means the lender isn’t looking at your house as a backup if you stop paying; they are looking at your income and your credit score. It’s cleaner, faster, and much less stressful in the long run.

| Loan Type | Collateral Required? | Typical Use Case |

|---|---|---|

| Personal Loan | No | Small to medium repairs, appliances, or quick upgrades. |

| Home Equity Loan | Yes | Major additions, structural changes, or large-scale remodels. |

| HELOC | Yes | Ongoing projects where you draw money as you need it. |

Comparing the Actual Numbers

Interest rates are the part that usually keeps people up at night. You want to know exactly what you are going to pay every month, and you want that number to stay the same so you can budget effectively. This is why many people gravitate toward fixed-rate loans rather than variable ones.

The rates you see advertised can be a bit deceptive. They often represent the absolute best-case scenario for someone with perfect credit. If your score is in the 700s or 800s, you’ll have a much easier time finding a deal that doesn’t sting. If your credit is just “okay,” expect to pay a bit more for that convenience.

Take a look at what different institutions are offering right now to get a sense of the market. For example, Wells Fargo offers unsecured home improvement personal loans with rates starting as low as 6.74%. While that sounds great, you have to check if you qualify for that specific rate before you get your heart set on it.

It is important to compare more than just the APR. You should also look at the term length. If you spread the payments over a longer period, your monthly bill is lower, but you will end up paying much more in total interest over the life of the loan. It’s a classic trade-off: do you want more breathing room today or more money in your pocket tomorrow?

Some lenders offer very flexible terms to help you manage your cash flow. For example, U.S. Bank allows current clients to choose a repayment period between 12 and 84 months, though for many, a shorter term is better for the bottom line. You might even find a lender that offers a significant amount of cash without any of the usual headaches associated with traditional banking. If you are looking for ways to manage your finances effectively, checking out a site like texasloanstoday.com can give you a broader perspective on different lending models available to you.

The Hidden Perks of Unsecured Funding

One of the biggest benefits of a personal loan for home improvement is the speed. If your water heater explodes on a Tuesday, you don’t have time to wait three weeks for an appraiser to visit your house and another month for the bank to process a home equity line of credit. With a personal loan, you can often have the money in your account within a few business days.

There is also a certain level of freedom that comes with an unsecured loan. Once the money hits your bank account, the lender doesn’t care if you spend it on a new roof, a fancy new stove, or a deck for the backyard. They don’t require receipts, and they don’t need to inspect your work to ensure you are actually doing the renovations they intended to fund. They just want their monthly payment.

However, don’t think this means you can be reckless. Even though there is no collateral, the debt is still very real and it will show up on your credit report. If you take out $30,000 for a kitchen remodel and then realize you can’t afford the monthly payment, your credit score will take a massive hit. Use the money for the house, not for a vacation you can’t afford.

Are you prepared for the monthly commitment?

A lot of people forget that a loan is a weight. Even though it feels like “free money” when the contractor is standing in your kitchen asking for a check, it is a monthly obligation that stays with you for years. You need to be certain that the value added to your home, or even just the utility of the repair, justifies the monthly outflow from your checking account.

Finding the Best Fit for Your Project

Not all loans are created equal, and the “best” loan depends entirely on your specific situation. If you have a high credit score and need a quick $10,000 to fix a deck, a personal loan is almost certainly the winner. It’s fast, it’s easy, and it doesn’t put your house at risk.

If you want more specialized options, some lenders cater to specific groups. For example, Navy Federal provides various options for their members, including home equity loans and other financing for renovations and emergency repairs. They understand their community’s needs, which can sometimes lead to more tailored service than a massive national bank.

- Personal Loans: Best for quick repairs and small-to-medium upgrades like appliances or flooring.

- Home Equity Loans: Best for large-scale structural changes where you have significant equity to leverage.

- HELOCs: Best for ongoing, multi-phase projects where you need to draw funds as work progresses.

- Credit Cards: Best for very tiny tasks, but often carries the highest interest rates.

I always tell people to check for origination fees. Some lenders will charge you a fee just for the privilege of taking out the loan, which is essentially a hidden cost that eats into your renovation budget. Discover, for instance, offers up to $40,000 for home remodel or repair loans without charging an origination fee. That is a significant detail when you are trying to make every dollar count toward your new cabinets.

You should also look at the APR, which includes both the interest rate and any mandatory fees. A loan with a 6% interest rate and a 3% origination fee might actually be more expensive than a loan with a 6.5% interest rate and no fees. Do the math before you sign anything. It is better to spend an hour comparing numbers now than to spend two years paying for a mistake.

Is This Worth the Debt?

The big question most people ask is: “Will this renovation actually pay for itself?” This is a complicated question because it depends heavily on your local real estate market and the type of work you are doing. A brand-new, high-end kitchen in a modest neighborhood might not give you a 1-to-1 return on investment, but it will make your life much more enjoyable every single day.

If you are fixing something broken, like a roof or a heating system, you aren’t really looking for a return on investment; you are looking for damage control. In those cases, the loan is a tool to prevent further decay of your most valuable asset. If you are upgrading, you are investing in your quality of life. Both are valid, but they require different ways of thinking about the money.

You might be worried that taking on more debt during an uncertain economy is a mistake, but remember that a well-maintained home is a hedge against inflation. As the cost of materials and labor continues to rise, fixing your house now with today’s money might be cheaper than waiting two years and facing even higher prices. It’s about balancing the risk of debt against the certainty of rising costs.

Questions people ask

Can I use a personal loan for home improvements?

Yes, personal loans are unsecured funds that can be used for any legitimate purpose, including home renovations and repairs.

Is a personal loan better than a home equity loan for remodeling?

Personal loans offer faster funding and no collateral requirements, whereas home equity loans typically have lower interest rates but require your house as security.

How much can I borrow for home improvement via a personal loan?

Loan amounts vary by lender but typically range from $1,000 to $50,000 depending on your credit score and income.

Will a personal loan for home repairs affect my credit score?

Applying for a loan may cause a small, temporary dip due to a hard inquiry, but consistent on-time repayments can improve your score over time.

Are there tax benefits to using a personal loan for home improvements?

Generally, personal loans are not tax-deductible, unlike home equity loans which may offer interest deductions if the funds are used to improve the secured property.